Mastering Cost of Carry: Forward & Reverse Conversions Explained

Deep dive into cost of carry, forward conversions, reverse conversions, and how to use these strategies with the ApexVol platform.

What You'll Learn

- Understand how cost of carry affects options pricing

- Learn to identify forward conversion opportunities

- Execute reverse conversions for synthetic positions

- Use ApexVol's analytics to spot pricing inefficiencies

Video Summary

What is Cost of Carry?

Cost of carry is a fundamental concept in options pricing that represents the net cost of holding a position over time. It includes interest rates, dividends, and storage costs. Understanding cost of carry is essential for identifying arbitrage opportunities and pricing synthetic positions accurately.

Forward Conversions

A forward conversion combines a long stock position with a long put and short call at the same strike and expiration. This creates a risk-free position that should earn the risk-free rate minus dividends. When the market misprices this relationship, arbitrage opportunities emerge.

Reverse Conversions

The reverse conversion is the mirror image: short stock, short put, long call. Professional traders use this to exploit situations where put-call parity is violated. We demonstrate how to use ApexVol's options chain and Greeks data to identify these opportunities in real-time.

Practical Application

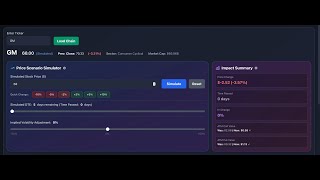

Using ApexVol's real-time data, we walk through identifying cost of carry discrepancies on SPY options. The platform's 340+ data points per ticker make it straightforward to compare theoretical vs. market prices and spot when conversions offer favorable risk-reward.

Related Guides

Try this with real market data

Analyze 5,500+ stocks with real-time options chains, IV analytics, and strategy P&L calculators.

7-day free trial · Card required · No charge if you cancel